Your Biggest Asset

Are you insuring your biggest asset?

With the majority of Australians still dangerously underinsured, is it time you reviewed your cover?

Jeff is a clean-living 53-year-old who exercises regularly, doesn’t smoke, enjoys a healthy diet and only indulges his love of good wine at the weekend.

Yet things changed suddenly for Jeff last year when he awoke one night to find he couldn’t breathe. His wife called for an ambulance and he was rushed to hospital, where he was taken into life-saving surgery following a heart attack.

After waking from his operation, Jeff was in deep shock. While he knew there was a family history

of heart disease, he had gone to great lengths to prevent the onset of the illness and had not properly thought through how his family would cope without him.

During his recovery, Jeff reviewed the life insurance component of his super and discovered that in the event of his death his family would receive just $300,000, which would barely pay off their mortgage. He had not taken into account daily living expenses, car loans, his daughters’ school fees, his wife’s low income or their inadequate savings.

Fortunately for Jeff his story is a positive one. Now in better health and back at work, he has spoken to a financial adviser and taken out additional life insurance, albeit at a significant premium following his heart attack. He and his adviser are also looking into critical illness cover, which would pay out

a lump sum should he suffer another sudden illness.

In Australia, Jeff’s story is not uncommon. In fact, surveys have shown Australia has much lower levels of insurance than other developed nations including the US and UK1[1]. The required level of life insurance is now about $680,000, while the typical default cover is about $258,000 – a significant gap2[2].

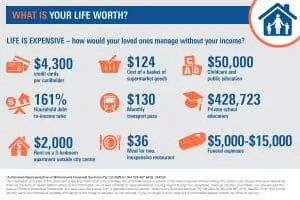

Could your loved ones make ends meet if you were unable to work or died? Here are some of the things you should consider:

- Mortgage or rent costs

- Daily living expenses – food, bills, transport

- Childcare

- School and university fees

- Other expenses – house repair costs, medical expenses

Make an appointment with your financial adviser to discuss your insurance needs and ensure

you are adequately covered.

*Authorised Representative of Millennium3 Financial Services Pty Ltd ABN 61 094 529 987 AFSL 244252

The information provided in this document is general information only and does not constitute personal advice. It has been prepared without taking into account any of your individual objectives, financial solutions or needs. Before acting on this information you should consider its appropriateness, having regard to your own objectives, financial situation and needs. You should read the relevant Product Disclosure Statements and seek personal advice from a qualified financial adviser. Millennium3 Financial Services Pty Ltd ABN 61 094 529 987 AFSL 244252. From time to time we may send you informative updates and details of the range of services we can provide. If you no longer want to receive this information please contact our office to opt out.

[1] Lloyd’s Global Underinsurance Report 2016

[2] Rice Warner Underinsurance Research Report 2014